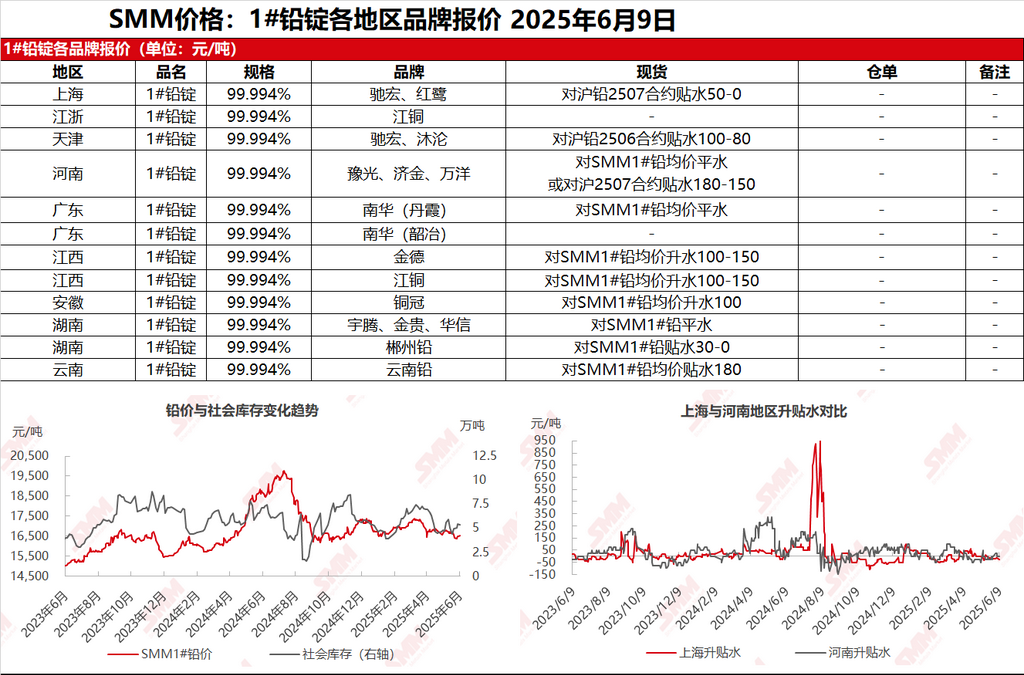

SMM News on June 9: In the Shanghai market, Chihong and Honglu lead were quoted at 16,675-16,740 yuan/mt, with quotations against the SHFE lead 2507 contract at discounts of 50-0 yuan/mt. SHFE lead continued to fluctuate, and suppliers shipped goods in line with market conditions. The discounts for some warrant cargoes widened compared to last Friday, while the discounts for cargoes self-picked up from production sites narrowed. Primary lead in major producing areas was quoted at premiums of 0-125 yuan/mt against the SMM 1# lead average price. Additionally, production cuts increased among secondary lead smelters, leading to scattered market quotations. Secondary refined lead was quoted at parity against the SMM 1# lead average price ex-factory. Downstream enterprises made just-in-time procurement only, with limited just-in-time demand, resulting in relatively sluggish spot order transactions.

Other markets: Today, the SMM 1# lead price rose by 25 yuan/mt compared to the previous trading day. Smelters in Henan quoted at parity against the SMM 1# lead average price ex-factory, while suppliers quoted at discounts of 180-150 yuan/mt against the SHFE lead 2507 contract ex-factory. In Hunan, smelters' quotations narrowed to parity against the SMM 1# lead average price ex-factory, and traders' quotations were at discounts of 30-0 yuan/mt against the SMM 1# lead average price ex-factory. In Guangdong, suppliers quoted at parity against the SMM 1# lead average price ex-factory. The center of SHFE lead's intraday movement shifted slightly higher. After some smelters' inventory levels declined, their quotation discounts narrowed. The supply of secondary refined lead had not yet fully recovered, and downstream procurement demand still leaned towards the primary lead market. Spot cargo transactions in some regions were moderate.